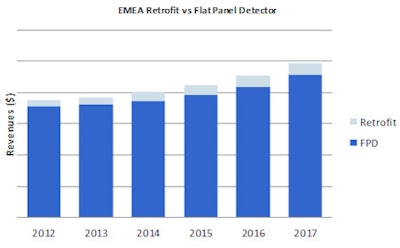

The retrofit flat-panel detector* (FPD) market has been in the spotlight over the last few years. In Europe, the Middle East, and Africa (EMEA), it was estimated to account for 3% of general radiography x-ray unit shipments in 2012, and the figure is forecast to increase to 5% by 2017. The retrofit market also has strong potential in EMEA, with lower cost digital x-ray systems being a high priority for hospital facilities to update existing analog systems.

Source: IHS.

Source: IHS.The greatest growth opportunity for retrofit is in emerging markets. Hospital providers here are using predominantly analog x-ray systems, providing a large installed base target for digital FPD retrofitting. Retrofit kits offer a less expensive solution and are forecast to more than double in size in emerging regions such as Central and Eastern Europe, the Middle East and Africa. Specifically in Central and Eastern Europe and Africa, fixed FPD x-ray systems remain too expensive for many hospitals, so retrofit kit solutions offer lower-cost access to full-digital x-ray imaging.

Russia has recently heavily invested in modernizing hospitals and general radiography x-ray systems were a key focus; therefore a large proportion of equipment has already been updated in Russia so the growth is not forecast to remain as high as in other emerging growth markets.

Smaller hospitals in Western European markets will also have high potential for retrofit due to the lower price. Currently, the price gap between computed radiography (CR) and digital retrofit FPD systems is still large enough to be significant to act as a limiting factor for retrofit uptake. Demand for retrofit x-ray equipment is predicted to have stronger growth when the price gap between computed radiography (CR) and retrofit FPD solutions narrows.

Source: IHS.

Source: IHS.The retrofit market often splits opinions among manufacturers, with some believing that retrofit solutions hold great potential long term, while others view retrofit as a "stopgap" solution. There is also a potential legal issue with retrofit. If an analog system is upgraded using a retrofit kit that has been made by a different manufacturer, where does the liability fall for system maintenance? This may cause future issues in terms of regulatory compliance, especially in the current era of increasing healthcare liability cases.

Market growth for retrofit may also be short lived, with some regions and providers choosing retrofit because of the lower prices compared with new FPD equipment; once the economy recovers and spending returns to normal, new x-ray systems will likely be the preferred option.

Wireless panels are becoming increasingly common in retrofit solutions. Wireless FPDs in retrofit kits improve flexibility of use (particularly in mobile system retrofit) and reduce risk of infections. Increased demand for wireless FPDs is also a significant driver of retrofit market development. Moreover, wireless is allowing a more "modular" approach to radiography systems, with an increasing trend to share panels across different x-ray rooms and mobile systems. There remain some concerns surrounding wireless panels, such as durability, connection issues, and battery life; image transfers from wireless digital panels can also be slow and systems can crash during transfer.

Competition

Retrofit x-ray kits were released into the market five years ago from a limited number of suppliers; 2012 saw an increased number of new suppliers targeting the booming retrofit market, due to increased demand from 2009 to 2011. Major manufacturers in this market currently are Agfa Healthcare, Carestream Health, Fujfilm Medical Systems, and Konica Minolta, who collectively accounted for 97.5% of the market in 2012.

The number of manufacturers selling into this market is also set to increase, with vendors such as ATLAIM and Claymount already releasing products into the market during 2012.

Manufacturers of FPD panels are set to broaden their product offering to include retrofit solution kits in the future, further intensifying competition. The increased competition will drive down prices and increase awareness of retrofit solutions in the market.

Big future?

Despite tough economic challenges in many developed countries in EMEA, the digital x-ray market still holds strong potential over the next five years. Retrofit will help drive digital x-ray in places where cuts have impacted purchasing and in emerging regions where fixed FPD system prices are too high for healthcare providers. Smaller clinics in Western Europe will also provide new market opportunities.

Market recovery from the recent poor economy could well limit the magnitude retrofit market growth long term in the mature markets of EMEA. New fixed FPD system shipments are forecast to pick up again as the economy improves in 2014 and 2015, having a potential impact on retrofit uptake.

Wireless FPDs will continue to drive growth in both retrofit and fixed FPD, with significant demand for wireless due to the benefits provided, including reduced risk of infection and the ability to share across different rooms and systems. More competition in both the wireless FPD market and wired is also predicted to drive prices down, increasing affordability of retrofit FPD systems for smaller clinics and hospitals.

So is the hype about retrofit to be believed?

In the short and midterm, probably not; the price gap for retrofit versus CR remains high enough to limit small hospitals and clinics from choosing retrofit, especially in the midst of liability concerns. Longer term and with declining FPD prices, it does offer a significant new market opportunity as a long-term replacement for CR.

*The data displayed above covers revenues and shipments generated from "retrofit kits;" these are considered as retrofit "systems" in such that they include both an FPD panel and a means of "adaption/integration" to the system being retrofitted. Therefore, only the branded manufacturer of "retrofit kits" is included in the analysis. Supply of FPD panels not part of a "retrofit kit," or supply of FPD panels to branded manufacturers of "retrofit kits," are not included in the above analysis.

Sarah Jones is an analyst at InMedica, now part of IHS.Inc (NYSE: IHS) specializing in x-ray technology markets. InMedica is a leading provider of market research and consultancy in the medical devices and healthcare iT industry (www.in-medica.com).

The comments and observations expressed herein do not necessarily reflect the opinions of AuntMinnieEurope.com, nor should they be construed as an endorsement or admonishment of any particular vendor, analyst, industry consultant, or consulting group.