MRI has been the flagship of diagnostic imaging since its conception in the mid-1970s. In 2012, demand for MRI equipment drove market revenues of $920 million U.S. (693 million euros) in Europe, Middle East, and Africa (EMEA) annually. Yet with increasing cost pressure across healthcare systems driving suppliers to focus on system cost, is there a risk of stalling innovation?

To answer this, some of the most widely tipped new areas and market trends are assessed below to predict the future role of MRI and its impact on the market.

','dvPres', 'clsTopBtn', 'true' );" >

Click image to enlarge.

The forecast development of EMEA MRI equipment. Source: IHS.

MRI in neurology

The rising impact and awareness of common neurological disorders has prompted substantial new focus on diagnosis with neurological MRI. The highest profile development has been the $100 million U.S. government 2014 budget funding for the Brain Research through Advancing Innovative Neurotechnologies" (BRAIN) program; other government initiatives also are widely predicted. While the majority of new funding will go into research centers, support for MRI as a screening tool for diseases such as multiple sclerosis (MS) and Alzheimer's disease is gathering momentum, suggesting demand for MRI as a screening tool is not too far afield. MRI technology has also made significant developments in terms of improved resolution with increasing magnet strength, a necessity for advanced neurological scans.

For manufacturers of MRI systems, this offers a significant opportunity, with many already running neurology-specific campaigns and partnering with key neurological thought-leadership centers in preparation. However, increased MRI adoption in this field will be dependent on three factors: first, lowering the cost of MRI services, particularly for 3-tesla and 7-tesla systems; second, increasing availability and access of MRI services, particularly in rural and community healthcare systems; and third, development of neurology-specific processing and analysis tools are required to increasingly automate diagnosis and improve efficiency.

Market outlook: Strong potential exists for global increase in MRI demand, though cost limitations and low accessibility will prevent significant growth in the short term.

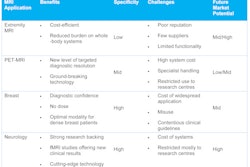

Extremity MRI

While not a new concept, extremity MRI has re-emerged as a cost-saving solution for high-throughput hospitals and clinics. As the majority of MRI systems are shared between clinical departments, removing the burden of extremity-only MRI (approximately a quarter of all scans) from full-body MRI can be advantageous. Furthermore, the increasing use of diagnostic imaging in musculoskeletal and specialist sports medicine applications is driving new usage for extremity-only MRI.

Keen to monopolize on this trend, many major imaging suppliers offer extremity MRI systems, including GE Healthcare, Hologic, and Esaote. However, strong demand has yet to materialize, with only 11% of total MRI unit shipped in EMEA in 2012 in the extremity MRI category. The greatest hurdle for suppliers remains the current economic climate, with private specialist clinics unwilling to invest in new systems due to cost restrictions. That said, the latest sweep of cost-saving reforms is changing healthcare provider focus toward alternative approaches and care models, thereby offering excellent potential for higher penetration of extremity MRI systems.

Market outlook: Limited uptake in the short term (2013-2015) due to current economic challenges, though midterm outlook remains positive with changing approach to utilization of imaging systems.

','dvPres', 'clsBtn', 'true' );" >

Click image to enlarge.

The forecast development of EMEA MRI equipment with different product mixes. Source: IHS.

PET/MRI

The release of the first fully integrated PET/MRI system has been touted as the next cutting-edge development for diagnostic imaging. However, various nonintegrated PET/MRI systems have been in circulation for a few years, with uptake and demand still relatively low. PET/MRI is often compared with PET/CT in terms of performance, with PET/MRI suggested to offer improved image resolution with no radiation dose. However, the high price of PET/MRI systems compared with PET/CT currently limits its use for all but specialist research centers.

One potential avenue for growth being explored is "virtual" PET/MRI. This involves obtaining images from currently installed PET/CT systems and conventional MRI, allowing PET data to be fused onto detailed MR images. In doing so, the need for the expensive integrated PET/MRI is removed, though the challenge of CT radiation still exists. The technology for fusion imaging already exists, facilitated by significant improvements in patient positioning and advanced visualization software. The greatest challenge will be convincing healthcare providers of the clinical accuracy of the "virtual" method, thereby requiring extensive trialing and comparison of "virtual" solutions versus integrated PET/MRI systems.

Market Outlook: PET/MRI outlook restricted to specialist research centers in the midterm; wide-scale adoption unlikely due to high cost of systems, though "virtual" approach could offer viable alternative in the long term after trialing.

Conclusion

As the above sections identify, current economic factors remain the greatest threat to new innovation of MRI in the next five years. This is particularly apparent in Western Europe, where crippling economic conditions are stalling new system installations. Despite this, such widespread change as a result of the economic situation could offer new growth opportunities in MRI. Healthcare providers increasingly need to asses and improve advanced imaging services, thereby offering opportunity for innovative new MRI technology. Success for suppliers will rely on the development of MRI solutions offering improvements in cost, efficiency, and workflow, while also improving clinical outcomes. Such a balance will be challenging to achieve in light of the current fiscal restrictions on healthcare; yet without such a focus, the long-term future of MRI innovation also may be at risk.

Stephen Holloway is the associate director of medical electronics research at inMedica, now part of IHS.Inc (NYSE: IHS). InMedica is a leading provider of market research and consultancy in the medical electronics industry (www.in-medica.com).

The comments and observations expressed herein do not necessarily reflect the opinions of AuntMinnieEurope.com, nor should they be construed as an endorsement or admonishment of any particular vendor, analyst, industry consultant, or consulting group.